Loan settlement is one of the most effective strategies for individuals struggling with overwhelming debt. If you’re finding it difficult to repay your loans due to financial hardship, job loss, or unexpected expenses, loan settlement can offer a practical solution to reduce your financial burden.

Unlike regular loan repayment, loan settlement allows borrowers to negotiate with lenders to pay a reduced amount as a one-time settlement. While it may impact your credit score, it can help you avoid legal complications and long-term financial stress.

In this comprehensive guide, we’ll walk you through everything you need to know about loan settlement, including its process, benefits, risks, and expert tips.

📌 Table of Contents

-

What is Loan Settlement?

-

How Loan Settlement Works

-

Types of Loans Eligible for Settlement

-

Benefits of Loan Settlement

-

Risks and Drawbacks

-

Loan Settlement vs Loan Closure

-

Step-by-Step Loan Settlement Process

-

Tips to Negotiate Better Settlements

-

Impact on Credit Score

-

When Should You Consider Loan Settlement?

-

Alternatives to Loan Settlement

-

Common Mistakes to Avoid

-

FAQs

-

Conclusion

What is Loan Settlement?

Loan settlement is a financial agreement between a borrower and lender where the borrower pays a reduced amount to close the loan. This usually happens when the borrower is unable to repay the full loan amount due to financial difficulties.

Instead of continuing with missed payments, penalties, and legal action, lenders may agree to accept a lower amount as a final payment.

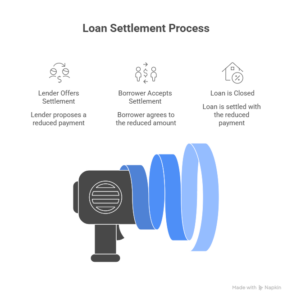

How Loan Settlement Works

The process of loan settlement begins when a borrower informs the lender about their inability to repay the loan. After reviewing the borrower’s financial condition, the lender may agree to a settlement.

Key Steps:

-

Borrower requests settlement

-

Lender evaluates financial hardship

-

Negotiation of reduced amount

-

Agreement on one-time payment

-

Loan marked as “settled”

Types of Loans Eligible for Settlement

Not all loans are ideal for settlement, but the most common ones include:

-

Personal loans

-

Business loans

-

Unsecured loans

Secured loans like home or car loans are less commonly settled because they involve collateral.

Benefits of Loan Settlement

Loan settlement offers several advantages for borrowers facing financial stress.

1. Reduced Debt Burden

You pay less than the total outstanding amount, making it easier to clear dues.

2. Avoid Legal Trouble

Settlement helps prevent lawsuits or recovery actions from lenders.

3. Faster Debt Resolution

Instead of long-term EMI payments, you can close the loan quickly.

4. Financial Relief

It gives you breathing space to rebuild your finances.

Risks and Drawbacks of Loan Settlement

While loan settlement can be helpful, it comes with certain downsides.

1. Impact on Credit Score

Your credit report will show “settled” instead of “closed,” which can lower your score.

2. Difficulty in Future Loans

Banks may hesitate to approve loans in the future.

3. Partial Financial Record

It indicates that the full amount was not repaid.

Loan Settlement vs Loan Closure

| Feature | Loan Settlement | Loan Closure |

|---|---|---|

| Payment | Partial | Full |

| Credit Score | Negative Impact | Positive Impact |

| Status | Settled | Closed |

| Future Loans | Difficult | Easier |

Step-by-Step Loan Settlement Process

Step 1: Assess Your Financial Condition

Understand your ability to pay and calculate how much you can offer.

Step 2: Contact Your Lender

Reach out to your bank or financial institution.

Step 3: Negotiate Terms

Discuss the amount and try to reduce penalties.

Step 4: Get Agreement in Writing

Always obtain a written settlement agreement.

Step 5: Make Payment

Pay the agreed amount in full.

Step 6: Collect Settlement Letter

This document proves your loan is settled.

Tips to Negotiate Better Loan Settlement Deals

-

Be honest about your financial situation

-

Offer a reasonable lump sum

-

Highlight financial hardship

-

Stay calm and professional

-

Consider professional help

For expert guidance, you can explore trusted financial platforms like

👉 https://www.thezavo.com/settle

Impact of Loan Settlement on Credit Score

Loan settlement can significantly affect your credit score. Credit bureaus like Experian or CIBIL record the loan as “settled,” which signals risk to future lenders.

However, you can rebuild your score by:

-

Paying bills on time

-

Using credit responsibly

-

Avoiding multiple loan applications

When Should You Consider Loan Settlement?

Loan settlement is suitable in situations like:

-

Job loss or income reduction

-

Medical emergencies

-

High-interest debt burden

-

Continuous loan defaults

If you still have the ability to repay the full amount, loan closure is always a better option.

Alternatives to Loan Settlement

Before choosing loan settlement, consider these options:

1. Loan Restructuring

Modify loan terms to reduce EMI burden.

2. Balance Transfer

Shift to a lower interest loan.

3. Debt Consolidation

Combine multiple loans into one.

4. Credit Counseling

Seek help from financial advisors.

Common Mistakes to Avoid in Loan Settlement

-

Ignoring lender communication

-

Not getting written agreement

-

Paying without confirmation

-

Settling too quickly without negotiation

-

Falling for scams

FAQs About Loan Settlement

1. Is loan settlement a good option?

It is helpful if you cannot repay the full loan, but it affects your credit score.

2. Does loan settlement affect CIBIL score?

Yes, it lowers your credit score and remains on your report.

3. Can I get a loan after settlement?

Yes, but it may be difficult initially.

4. How much can I save through loan settlement?

Savings vary but can range between 20%–60% of the total amount.

5. Is loan settlement legal?

Yes, it is a legal agreement between borrower and lender.

6. How long does loan settlement take?

It can take a few weeks to a few months depending on negotiations.

Conclusion

Loan settlement is a powerful financial tool for individuals struggling with debt. While it comes with certain drawbacks, it can provide immediate relief and help you regain control of your finances. The key is to use it wisely, negotiate effectively, and plan for a stronger financial future.

If you’re facing financial challenges, consider exploring professional help through trusted platforms like