Navigating the Geospatial Frontier: The Global GIS Market Outlook (2025–2032)

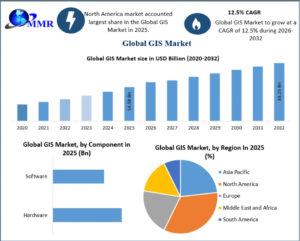

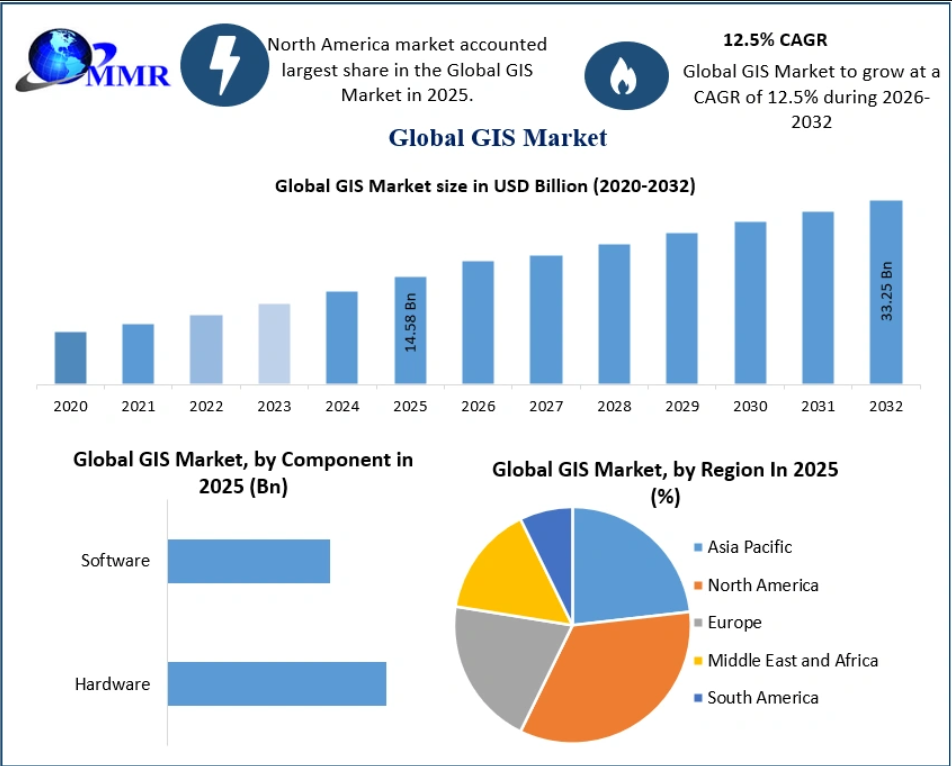

Geographic Information Systems (GIS) have transcended their origins as simple mapping tools to become the digital nervous system of modern infrastructure. As we move through 2026, the integration of spatial data into business and governance has become a prerequisite for operational success. The global GIS Market is currently on a high-growth trajectory, projected to expand from USD 14.58 billion in 2025 to USD 33.25 billion by 2032, maintaining a robust compound annual growth rate (CAGR) of 12.5%.

The Engine of Growth: Market Dynamics

The surge in the GIS sector is propelled by a convergence of technological maturity and rising global demand for data-driven precision. Several key factors are accelerating this adoption:

- Rapid Urbanization and Smart Cities: As urban populations swell, governments are turning to GIS-based infrastructure management to optimize city planning, disaster response, and transport networks.

- The IoT and Real-Time Analytics: The proliferation of Internet of Things (IoT) platforms allows businesses to capture real-time location data. This has shifted GIS from a static planning tool to a dynamic engine for location-based services and operational efficiency.

- Technological Integration: The adoption of LIDAR (Light Detection and Ranging) and cloud-based spatial data processing has lowered barriers to entry for high-precision mapping, enabling more frequent and accurate updates to geographic databases.

Despite this optimism, the industry faces hurdles. The high capital expenditure required for sophisticated hardware, software licensing, and long-term database maintenance can create a “cost barrier,” particularly for small- and medium-sized enterprises.

For further information, click the following link:https://www.maximizemarketresearch.com/request-sample/28729/

Segment Insights: Where Investment is Flowing

The GIS market is characterized by a diverse ecosystem of components and applications, each evolving to meet specific industrial needs.

Component Evolution

The market is divided between hardware (collectors, LIDAR, GNSS/GPS antennas, and imaging sensors) and software (desktop, server, mobile, and remote sensing applications). Software is poised for rapid growth throughout the forecast period, as cloud-native solutions and mobile GIS allow field workers to access and analyze spatial data instantaneously, a critical requirement for modern urban planning and transport management.

Functional Dominance

The Mapping segment continues to lead the market share. As industries ranging from defense and security to forestry and agriculture require sophisticated visualization tools, mapping software has become indispensable for retrieving, managing, and analyzing complex spatial data sets.

High-Growth Applications

While GIS is deeply entrenched in government and defense, the Agriculture sector is emerging as one of the fastest-growing application areas. By leveraging GIS for precision farming, producers can manage land resources with unprecedented accuracy, directly increasing yields while reducing overhead costs—a vital development for sustainable food production globally.

For further information, click the following link:https://www.maximizemarketresearch.com/request-sample/28729/

Regional Leadership: The North American Edge

North America currently stands as the dominant force in the global GIS landscape. This leadership is largely driven by consistent federal investment in geospatial infrastructure and the widespread integration of GIS software across government and corporate bodies in the United States and Canada. This regional dominance is expected to persist as agencies continue to prioritize digital mapping for civil and security operations.

The Competitive Landscape

The market features a mix of established global giants and specialized innovators. Industry leaders, including ESRI, Trimble Inc., Autodesk, Hexagon AB, and Bentley Systems, are heavily focused on developing ecosystems that bridge the gap between hardware sensors and cloud-based analytical software.

For stakeholders, the competitive arena is increasingly defined by the ability to offer end-to-end solutions—combining the data-gathering capabilities of high-end survey equipment with the analytical power of artificial intelligence and cloud computing.